China SignPost™ (洞察中国) #88: “China’s Public Hospital Governance Reforms are Setting the Stage for Corporatization”

Gabriel B. Collins and Andrew S. Erickson, “China’s Public Hospital Governance Reforms are Setting the Stage for Corporatization,” China SignPost™ (洞察中国) 88 (26 January 2015).

With appropriate legal and policy support, corporatization could begin within the next 2-3 years.

Key Points:

- China’s public hospital reform experiments thus far have laid a foundation for corporatization that is stronger than many observers believe.

- Public hospitals now are where the SOEs were in the 2-3 years before the 1994 Company Law was promulgated.

- Taiwan and Singapore offer potential models for corporatization and improving hospital governance structures, but we believe due to China’s sheer size, as well as its political realities, it will ultimately follow a “corporatization with Chinese characteristics” path.

- Without national guidelines on corporatization of hospitals, Beijing risks either perpetuating the skewed incentives that have helped spark social unrest and prompted the 2009 hospital reforms in the first place or having such a lack of legal clarity that investors balk at providing the full volume of capital that China badly needs in order to avoid having the public hospital system become a substantial drag on the national balance sheet.

- Events may begin to force policymakers’ hand if they do not move decisively to corporatize, or at least more clearly define the legal status of public hospitals in China. There are a sizeable number of local deals—primarily in 2nd and 3rd-Tier cities—where investors are taking majority stakes in public hospitals (typically ones suffering from some type of financial problems), with local governments as the minority partner.

- Introduction

China’s presently serious shortage of quality healthcare is a humanitarian black mark and also prompts a significant and rising trend of frustrated patients and their families resorting to violence against hospital staff and doctors.[1] Additionally, reigning in hospital-related costs, which comprise the lion’s share of healthcare expenditures in China, could help stimulate the consumer economy. The mechanism is that improving hospitals’ cost effectiveness and improving access to health insurance will reduce out of pocket medical costs, thereby incentivizing people to spend on other goods and services, instead of over-saving to self-insure against future medical problems.

Hospitals are the logical focal point because China’s healthcare system is extremely hospital-centric, with public hospitals delivering approximately 90% of the inpatient and outpatient care consumed in China today.[2] Chinese patients’ inclination to seek care at hospitals is reflected in a 2013 interview with then Vice Mayor of Shanghai Shen Xiaoming, himself a doctor. Vice Mayor Shen noted:

I have an electronic map in my office, and I can see in real time the traffic situation in all of Shanghai…For twenty-four hours in the day, the most congested spots in Shanghai are the front entrances of Ruijin Hospital, Huashan Hospital, and Zhongshan Hospital [in Central Shanghai].[3]

The situation is similar more broadly across China. In 2012, close to two-thirds of China’s total healthcare spending occurred in the hospital sector, as opposed to the 30%-to-45% seen in many OECD countries.

This paper aims to analyze the evolving organizational structures used by hospitals in China and assess how economic reform pressures may have influenced this evolution. State involvement in the hospital sector has, in many ways, played out very differently than in other key industrial and financial sectors. Indeed, while the government worked hard to retain control of key “commanding heights” sectors of the economy such as oil, steel, and shipbuilding during the Reform Era, it has largely left hospitals—a massively strategic sector—on their own. In doing so, it created a system where government ownership co-exists with a distinctly private set of operational incentives, such as the need to sell pharmaceuticals, lab tests, and other services to stay afloat financially.

Hospital organizational structures offer a unique analytical opportunity because unlike the late Qing Self-Strengthening, and PRC corporate buildout and the SOE reforms post-1978, hospitals do not need to “create” a market. The market of Chinese citizens who need healthcare is already booming, and has been for some time. It is also changing focus. During the Mao years, infectious diseases, child mortality, and other common developing world issues were the main challenges China’s healthcare system faced. Many of these could be dealt with at low cost by the legion of “barefoot doctors” then dispatched to the countryside.

Yet since 1978, and especially in the last decade, China has experienced a rising tide of serious chronic illnesses such as cancer and diabetes that are in many ways direct products of prosperity—such as sedentary lifestyles and richer diets—as well as externalities of growth, such as cancers caused by industrial pollution.[4] These ailments are typically beyond village clinics’ ability to handle and instead require more sophisticated treatments that are usually administered in hospitals by doctors trained in Western-style medicine. In this new environment, the hospitals’ task is to find the ways to best serve that market through more accessible and affordable healthcare.

As the Central government re-engages with healthcare and hospitals with a focus not seen since the early Mao period, the question arises of whether or not public hospitals will be corporatized the way SOEs were. China’s public hospitals are now approaching a crossroads similar to that which the large SOEs faced in the late 1980s and early 1990s and the likelihood of public hospitals being granted independent legal personality and allowed to corporatize is rising rapidly.

Corporatizing hospitals impacts legal structure and status of hospitals and would ideally have a direct positive effect on operational efficiency. It will also aid the State’s campaign to attract private sector infusions of capital and expertise into the hospital sector by making it easier to define the value of potential investments. Attracting new investment and private sector capital into the public hospital sector will be especially important in coming years as existing hospitals, many of which were built in the 1950s, approach the end of their useful service lives and require replacement or substantial remodeling.

In light of these challenges and opportunities, this report aims to clarify the Chinese public hospital sector’s place on the road to corporatization, how the situation is evolving, and what this means for investors, scholars, and policymakers wishing to engage this vital segment of China’s healthcare value chain.

- Historical Landmarks for Public Hospitals in China

When China began to undertake broad economic reforms in the late 1970s, it enjoyed one of the most effective and cost-efficient healthcare systems in the developing world.[5] Between 1960 and 1980, the average PRC resident’s life expectancy rose from 43 years to nearly 67, an improvement in human wellbeing unsurpassed anywhere else in the world during that time, and one which sprang largely from significant improvements in the provision of public health services.[6]

Along with economic reforms, the Chinese government also began to reform the country’s public hospital system (which at the time included virtually all of China’s hospital capacity). This section of the paper will discuss the three key waves of reform that the government has unleashed on the hospital sector, with a specific focus on how they have affected the operations of China’s public hospital sector. Wave One spanned 1980-2003, Wave Two spanned 2003-09, and Wave Three covers 2009 to the present time.

Wave One: 1980-2003

This reform wave focused on introducing market incentives to public hospitals, primarily by reducing government subsidies to hospitals and giving them autonomy to earn income from selling pharmaceuticals and services. These reforms first affected the rural areas, and only much later came to affect larger urban hospitals.

In 1992, the Ministry of Health grated hospitals substantial financial autonomy, allowing them to charge for services, sell pharmaceuticals at a profit, keep surpluses they generated, and bear responsibility for debts and operating losses.[7] In essence, Beijing wanted to move the costs of hospital operations off of the government balance sheet as economic reforms deepened. The result was that unless a public hospital was affiliated with a deep-pocketed entity such as a large university or the military, it had no choice but to become a quasi-commercial entity that happened to be publicly-owned. As one Chinese analyst colorfully puts it “the hospitals relied on the government to get built, but had to rely on themselves to eat” (建设靠国家, 吃饭靠自己).[8]

“Relying on themselves to eat” and the ensuing commercialization of public hospital operations rapidly created a number of un-intended consequences that the state became increasingly unable to ignore. Most critical, access to quality healthcare declined as the combination of reduced insurance coverage (a product of other healthcare sector reforms) and higher charges for drugs and procedures priced many Chinese out of the market. Out of pocket payments rapidly came to comprise the lion’s share of total healthcare expenditures, reaching an apogee of 60% in 2001 before a second wave of reforms began to stem the expense burden directly borne by patients.[9]

Wave Two: 2003-09

The 2003 SARS epidemic played a pivotal role in highlighting weaknesses across China’s healthcare system, particularly on the governance front, and helped focus public outcry in a way that grabbed policymakers’ attention and helped prompt additional reforms.[10] In addition, the accession of a new set of leaders to power also presented an opportunity for them to capitalize politically by promoting healthcare reforms.

However, the reforms between 2003 and 2009 focused primarily on increasing health insurance coverage, rather than on reforming the public hospital system. For instance, in 2003 the government established the New Rural Cooperative Medical Insurance (NRCMI) for China’s rural population, expanded the Urban Employees Basic Medical Insurance (U-Employee) for urban employees, and finally, established the ‘rural medical assistance’ for impoverished rural residents.[11]

Wave Three: 2009-Present

In April 2009, the Chinese government announced the largest and most focused set of healthcare reforms since perhaps the Mao era. Pilot hospital reforms comprised one of the five key pillars of the 2009 program.[12] The State Council Reform Office followed up in 2010 by issuing reform guidelines, after which the government chose 745 public hospitals in 17 counties and 37 pilot provinces and cities in which to experiment with new governance and operational practices.[13] This is a broad sample size and represents approximately 5.5% of China’s total public hospitals—a meaningful number that is large enough to create a groundswell if reform measures currently being tried out end up succeeding.

- Current Legal and Ownership Status of Public Hospitals in China

Legal Status of Hospitals in China

Hospitals in China presently fall into two broad categories of legal personality. One is the “enterprise legal person” used in the 2005 Company Law. Enterprise legal person status governs private hospitals, whether Chinese or foreign-invested, as well as joint ventures. For example, Changning District Central Hospital in Shanghai (foreign-invested) and Changcheng Hospital in Foshan, Guangdong (Chinese-invested) are both enterprise legal persons operating as limited liability companies.[14]

All public hospitals in China are currently classified as “Enterprise Danwei Legal Persons” (事业单位法人). [15] The “enterprise danwei legal person” class is a legacy of the old SOE period, when the firms controlled a whole constellation of assets such as hospitals, theaters, and schools that were not directly connected to the core focus of the enterprise. While corporatized SOEs are now “enterprise persons,” as recognized in Article 3 of the 2005 Company Law, public hospitals still remained burdened with the weak Enterprise Danwei legal personality.

Legal structure and ownership status become less clear (and much more adventurous for the risk seeking) once we transition over to public hospitals. The matter is both intellectually interesting and deeply useful from a policy and commercial perspective. Chinese analysts say the legal status of public hospitals is currently vague and that this can create major problems because the legal lines of demarcation between hospitals and the government bodies working with them and, to some extent funding them, is not clear.[16]

Despite the current problems, there should be a path for resolution. Public hospitals’ inherent characteristics do not logically preclude them from enjoying independent legal personality under Chinese law. Most public hospitals operate as quasi-private entities, are effectively self-funding, possess increasing internal competence to make operational decisions within a market context, and their assets can be transferred and even privatized. In short, they share many traits with existing SOEs in China, which the law bequeaths with independent legal personality as “enterprise legal persons.”

Indeed, as early as 2003, public hospital assets had their value defined and were privatized. In 2003, United States China Hospital Inc. purchased the “entire rights, interests, and liabilities” of Anqiu City People’s Hospital. The agreement included a transfer of land rights and a pledge by the purchaser to continue improving the office buildings and hospital rooms to make a “garden-style hospital.”[17] These data points all overwhelmingly point to a transaction based on buying actual bricks and mortar formerly owned by the state, as opposed to management rights only.

The Anqiu deal is noteworthy because the buyer dealt directly with the State Asset Management Bureau of Anqiu City, who functioned as the “owner” of the hospital assets. Other examples exist of local state asset management bodies being willing to offload hospitals. For instance, the Beijing State Owned Assets Management Co. notes that in recent years it has helped “dispose of” at least three public hospitals: Beijing University People’s Hospital (北京大学人民医院), the Health Ministry’s Beijing Hospital (卫生部北京医院), and the Beijing University No. 3 Hospital (北京大学第三医院).

Ownership Status of Hospitals in China

Hospital ownership in China splits into two primary levels—physical asset rights (ownership of bricks, mortar, medical equipment, employees) and management rights. Physical ownership typically resides with the investors for private facilities and with the state for public hospitals.

The management rights appear to be effectively severable, allowing the state to retain ownership of the building, employees, and so on; but allowing a private management company to purchase management rights that allow it to try and wring efficiencies out of hospital operations. Indeed, making management rights severable allows the state the option of “privatization lite” where the government retains ownership of the physical hospital itself, but can sell or rent out the management rights for all or part of the hospital’s operational functions to a market-driven private actor.

Management Companies Highlight Murky Delineation of Property Rights in Public Hospitals

The management companies present interesting legal questions because some, such as Golden Meditech are totally private; while others, such as Sinopharm, are SOEs or wholly-owned subsidiaries of SOEs.[18] For instance, Sinopharm Midland Hospital Management Company manages five hospitals in Henan province: Xinxiang Central Hospital (新乡市中心医院), Xinxiang No. 2 People’s Hospital (新乡市第二人民医院, Xinxiang Maternal and Child Healthcare Center (新乡市妇幼保健院), Xinxiang Hospital of Chinese Medicine (新乡市中医院), and Xinxiang No. 3 People’s Hospital (新乡市第三人民医院).[19]

The five hospitals are all public hospitals, and have enterprise danwei legal personality.[20] Sinopharm Midland Hospital Management Company gained the rights to manage the hospitals after the Xinxiang City Government and Sinopharm Group Company (Midland’s ultimate parent) reached an agreement with each other.[21] There do not appear to be publicly available data on what the consideration for the agreement was, which raises significant questions about what property rights, if any, the management company may have acquired beyond a right to manage operations. One possibility is that these management companies are following an approach similar to that used by Phoenix Healthcare, perhaps China’s largest private hospital management company. Phoenix uses a so-called “invest-operate-transfer” (“IOT”) model, under which it agrees to make a fixed investment to improve hospital facilities as well as clinical services of a hospital “in exchange for the right to manage and operate that hospital and…receive performance-based management fees and the ability to supply pharmaceuticals, medical devices and medical consumables for a period ranging from 19 to 48 years. If the relevant IOT agreements are not renewed or extended after such period, the management rights will be transferred back to the hospital owner.”[22]

The IOT arrangement in many ways appears to be kicking the can down the road, as it still does not address the fundamental underlying legal question of who owns what. This lack of clarity is reflected by the fact that early investors in public hospitals have already had to deal with a range of entities, including the Ministry of Health (“MOH”), local State Owned Assets Supervision and Administration (“SASAC”) offices, and city governments in order to broker deals, and each city often poses a different contractual scenario.

Given that hospital’s legal status is intimately intertwined with the evolving ownership structures, the next section examines how new reforms are changing the public hospital governance framework in ways that move the sector closer to corporatization.

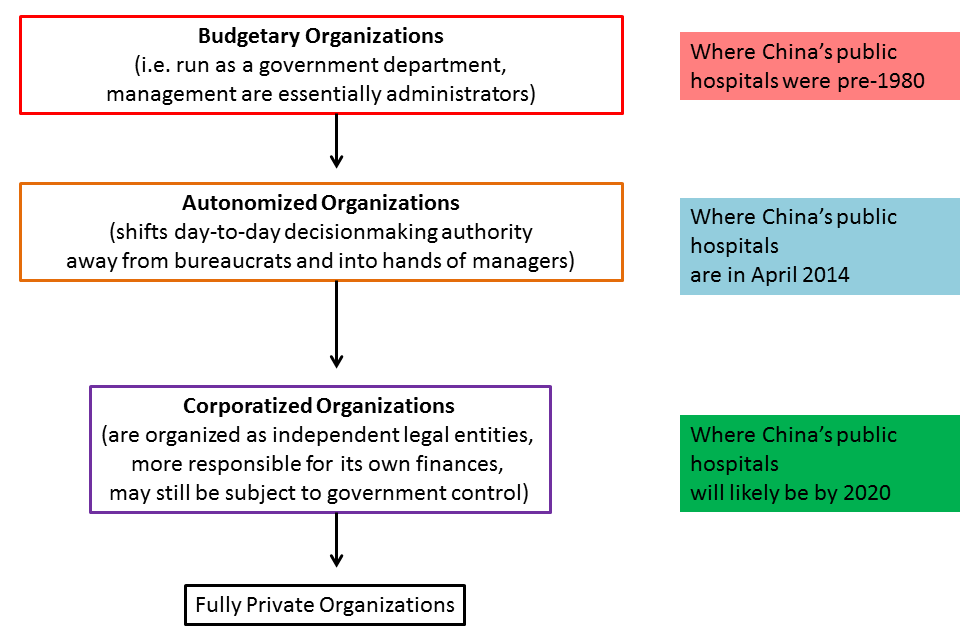

- Where Chinese Public Hospitals are Now on the Corporatization Spectrum

The most appropriate classification for most Chinese public hospitals now would be “autonomized organizations.” Essentially, this means they are in a state where they are still government-controlled, but have, or are in the process of, shifting meaningful decision-making authority into the hands of those actually managing the assets, rather than those pushing paper in a far-away ministry office (Exhibit 1).[23]

Exhibit 1: Past, Current, and Projected Status of Chinese on Corporatization Spectrum

Source: Preker and Harding, China SignPost™ assessments

- Why Haven’t Public Hospitals in China Corporatized Yet?

Key Chinese healthcare officials—up to the ministerial level—have expressed support for public hospital governance reforms, but opposed “corporatization.” Such views appear to be driven by a fundamental misconception—namely that “corporatization” diminishes an asset’s ability to be used with an emphasis on the public good. The October 2009 statement of the Vice Minister of Health, Ma Xiaowei, offers a clear example of this misunderstanding:

State-owned assets can gain financial value from reforms, while public hospitals have to protect the public interest. Reforms can help make healthcare gains but we should thoroughly understand the difference between the two [increasing asset value versus protecting the public interest]. We should be mindful of lessons but not proceed indiscriminately and must avoid conflating the grant of legal personality with actual corporatization. (国有企业以国有资产保值增值为改革目标,而公立医院则以保证公益性、提高健康绩效为改革目标,在改革中必须充分认识二者的差异,借鉴而不照搬,避免公立医院‘法人化’演变为‘公司化).[24]

It very much appears that Vice Minister Ma is equating “corporatization” with full-on “privatization.” Yet corporatized entities can still put state or public interests first and foremost in their operations. Indeed, Ma’s statement is actually deeply ironic given the ways that China has used, and continues to use, corporatized (sometimes even publicly-traded) SOEs to pursue national interest-oriented projects in a variety of sectors.

For their part, potential domestic investors have a more nuanced view, but still admit that unclear delineation of property rights plus hospitals’ critical social function pose real challenges that hinder investment, but which would also need to be addressed for successful corporatization to occur. For example, Feng Suqiang, a managing director at private equity firm Zero2IPO Group, notes that commercial (read: hospital operators) and private equity investors alike must tread carefully due to lack of clarity with respect to property rights, as well as the need to balance profitability with social duties after an investment is made in a public hospital.[25]

Opposition to corporatizing public hospitals in China also overlooks the reality that two core motivations for corporatization are arguably already deeply embedded in China’s public hospital sector. First is the idea that by granting hospitals the right to retain residual revenue, managers have incentive to ensure that the hospital operates more efficiently.[26] For more than two decades, public hospitals in China have been permitted to keep the surpluses they generate and are also responsible for any debts or operating losses they may incur.[27]

Second is giving hospital managers greater decision-making autonomy creates more latitude for them to optimize hospital operations.[28] Chinese public hospital managements arguably have not yet been granted broader residual rights to control, namely the rights to “make any decision regarding as asset’s use not explicitly contracted by law or assigned to another by contract.”[29] Many areas remain where public hospitals in China are still sufficiently entwined with—and constrained by—bureaucratic authorities, that they are some distance from being able to be called “corporate.” That said, it is very likely that if the Chinese government decides to allow hospital corporatization, it will proceed much more smoothly and rapidly than it did when the first SOEs were corporatized.

There are several reasons for this. First, the hospitals already have substantial experience operating as quasi-market entities and are not being forced to move directly from planned economy operations into a market environment. Second, the legal framework, regulatory knowledge base, and service elements (bankers/lawyers, etc.) that are needed to breath functional life into corporations already exist in decent measure in China owing to the prior SOE reforms. Third, Chinese policymakers can examine lessons from other Asian political entities, namely Taiwan and Singapore, which share meaningful cultural similarities with the PRC—and which have more evolved public hospital systems than the PRC does at present.

Path One—Taiwan (not likely)

Of Taiwan’s roughly 500 hospitals, approximately 80% are privately owned, according to 2012 Ministry of Health and Welfare data.[30] The remaining public hospitals are primarily controlled by either the Ministry of Health and Welfare or the Taiwanese military. Taiwan’s public hospitals are not corporatized and instead are directly administered by the government.

The Taiwanese model is likely not appropriate for the PRC given Beijing’s policy objectives. First and foremost, roughly 90% of PRC hospital capacity lies in the public hospitals, which are likely to remain the focal point of care for decades to come. Second, part of the reason the PRC is seeking to reform public hospital governance is that the leadership wisely recognizes that trying to govern thousands of hospitals—each of which are very important locally—from the center is unworkable if the system is to be made more efficient and effective.

Third, much of Taiwan’s private hospital capacity is controlled by large corporations, whose wealthy entrepreneur founders have established private foundations that control and manage the hospitals. Among these is Chang Gung Memorial Hospital, which has 9,000 beds in its system and is one of the world’s largest hospital organizations.[31]Chang Gung was established by the founder of Formosa Plastics after his father (named Chang Gung) died of an intestinal obstruction that could have been easily remedied with access to modern medical care.[32]

A private hospital sector is emerging in China as reforms progress, but in contrast to Taiwan, private providers are unlikely to become the core of healthcare provision in the PRC. Moreover, China’s largest corporate bodies—the core SOEs—are assiduously trying to rid themselves of hospitals that are a drag on corporate finances and distract from the firms’ core businesses.

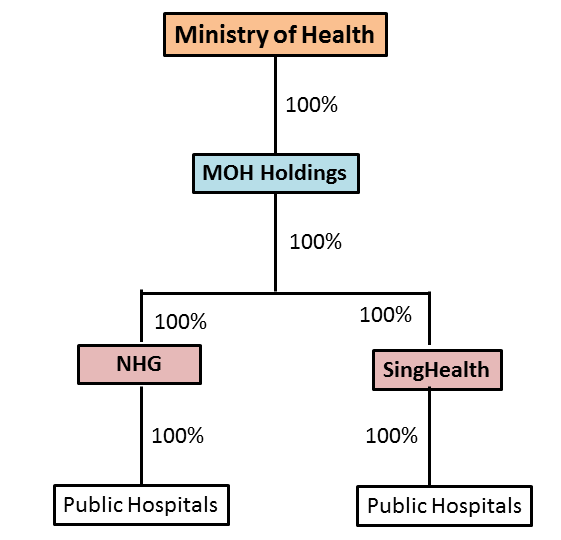

Path Two—Singapore (more promising)

In contrast to Taiwan, public hospitals dominate Singapore’s system, providing ¾ of hospital beds.[33] Furthermore, Singapore chose to corporatize its public hospitals. As Ramesh describes, the primary phase of corporatization occurred between the mid-1980s and the early 1990s, after which the government asserted more robust government “direction” of hospital activities.[34] The Singapore government’s primary rationale for imposing stricter direction was that the rise in competition following corporatization had also driven up healthcare costs.[35]

Singapore selected a hospital management structure in which the government owns a holding company called MOH Holdings.[36] In turn, MOH Holdings owns NHG and SingHealth, which between them control all public hospitals in Singapore, which are structured as separate private companies (Exhibit 2).[37]

Exhibit 2: Singapore Private Hospital Ownership Structure

Source: “Autonomy and Control in Public Hospital Reforms in Singapore,” MOHH, SingHealth

The Singaporean example is noteworthy, both for the potential insights it offers into paths China could take, as well as key distinctions that will make China’s hospital reform program very different. In the similarities column, China also relies on public hospitals to provide the bulk of care. Likewise, Singapore also faced—and is competently addressing—corporatized hospitals’ propensity to act as quasi-private profit seekers at the expense of providing high quality, accessible care. Finally, both countries have semi-authoritarian governments whose relevant top officials are on balance arguably more technically competent than most of their counterparts in Western democracies.

Several differences exist as well. First, China’s hospital system is an order of magnitude larger than Singapore’s, with commensurately greater administrative complexity in terms of achieving final solutions when implementing policies. As a subset of the scale problem, China’s vast expanse means there will likely be enduring disparities in healthcare quality, particularly between rural areas and inland urban areas vis-à-vis their coastal cousins (where most of China’s top hospitals are located).

Second, in relative terms, China’s population faces much greater burdens from complex chronic diseases such as diabetes and cancer than the Singaporeans do, a reality that will likely substantially increase the relative demand for hospital-centric care in China. Third, China’s current mélange of regional and city-level administrative experiments in hospital governance and overall thrust of localizing hospital governance may present political challenges in terms of standardizing healthcare costs and quality in practice.

Fourth, China’s population is aging rapidly, creating a situation whereby the country will most likely “get gray” before it gets rich, which increases the insurance cost burden on the remaining young people who then must bear a proportionally larger burden to ensure their aging parents, aunts, uncles, etc. Finally, China’s existing public hospital problems are serious enough that Beijing will not have the luxury of time Singapore enjoyed (15 years to corporatize all public hospitals).

Path Three—Public Hospital Governance Improvements with Chinese Characteristics

A huge set of related questions looms over China’s public hospital reform campaign—will Chinese public hospitals be corporatized? Do they need to be corporatized in order to achieve Beijing’s reform objectives? Might there be reforms short of corporatization that are conducted first to lay the groundwork for later corporatization? Will public hospitals in China be corporatized in a way that reflects local characteristics? Based on the research, analysis, and Chinese-language source evidence outlined here, the short answer to these questions is “yes.”

At present, public hospital ownership and governance models are in flux in China. A great amount of experimentation is under way, as has been for more than a decade. Quiet structural reform experiments began in 2002 in Shanghai (addressed in greater detail below) and more followed in other locations, but the real wave came following the April 2009 promulgation of the “Medicine and Healthcare Systemic Reform Near-Term Implementation Plan for 2009-2011” (医药卫生体制改革近期重点实施方案 (2009-2011年).[38]

Exhibit 3 (below) highlights (1) of how diverse the public hospital governance reform attempts are and (2) how many of them predate by several years the 2009 official blessing for reforms.

Exhibit 3: Sample China Public Hospital Governance Reforms

Source: Zhang et.al, “Analysis of Shanghai’s public hospital governance structure with the Preker-Harding model.” 2013

The themes which most deeply permeate the governance reform experiments center on creating city-level management structures—a clear signal that the ultimate policy results stand a good chance of increasing local governments’ influence over, and involvement with, public hospitals in their jurisdictions. This tracks with the assessment of Wang Hufeng from the Health Reform and Development Center in Beijing, who notes that three primary models of reform aimed at separation of ownership and management are emerging in China’s public hospital sector, all focused on city-level political entities.[39]

The reform packages also emphasize separations of ownership and management. The weaker legal personality given to public hospitals makes the current governance reforms aimed at separating ownership and management very important. Indeed, Li Weiping and Huang Erdan, senior analysts at the Ministry of Health’s Institute of Health Economics have written that the 管办分开 (guanban fenkai, or “separation of control and operations”) campaign should be thought of as an action that effectively confers more robust legal personality upon public hospitals.[40] Moreover, it is telling that these two well-positioned analysts also believe moves to separate ownership and governance actually reinforce legal personality at three key points in the public hospital system: individual hospitals, groups of affiliated public hospitals (where this applies), and new overarching hospital governance structures being created primarily at the municipal level.[41]

One of the core challenges in implementing guanban fenkai will be figuring out what powers continue to reside in public hospital Party Committees. Most, if not all, public hospitals (certainly the large ones) have Party Committees embedded within them. There appears to be very little discussion of what the full extent of these committees is, but there is reason for concern that as more operational power is granted to local-level bodies, the Party Committees may become a backdoor trump card that the Central or Provincial governments can use to hinder reforms or actions with which they come to disagree. This would be akin to the veto power that Party Committees can exert within the large SOE banks or enterprises governed by the 2005 Company Law, where Article 19 leaves a large space for the Party to serve as a “checking” mechanism versus management.

The vague manner in which some hospitals define the role of their Party Committees should grab the attention of potential investors, who should be aware of this potential “dormant volcano.” For instance, Huashan Hospital, one of Shanghai (and China’s most capable) says that its Party Committee exists to carry out a range of duties, including “faithfully implementing whatever work the Party leadership may hand down” (…认 真完成党委领导交办的其它各项任务).[42] In a similarly broad and open-ended manner, Leshan People’s Hospital (serving the prefecture-level city of Leshan in Sichuan) says its Party Committee functions as a “comprehensive social order governance and peaceful development small working group” (社会治安综合治理和平安创建工作领导小组).[43]

Guanban fenkai is also important because if the policy goals are implemented with sufficient speed, Chinese public hospitals may undergo significant governance changes before they achieve independent legal personality. This would put them on a different path than core SOEs, which were granted independent legal personality in 1986 by the General Principles of Civil Law, but did not begin significant governance reforms until 1992, when the State Council promulgated the Regulation on Transforming the Management Mechanism of the Industrial Enterprises Owned by the Whole People.[44]

- Public Hospital Governance Reforms: Steps Toward Corporatization?

China’s latest round of hospital reforms points to a trend of making hospitals more “independent,” while also more clearly delineating lines of authority and control and clarifying public hospitals’ relationship with the political power structure. Basically, this is being done by formalizing a devolution of significant governance authority and putting more power in the hands of new municipal health bureaus and other administrative bodies specifically tasked with overseeing public hospital operations. This analysis will specifically emphasize a case study of governance structures being adopted by Shanghai for its public hospitals.

Public Hospital Governance Reforms in Shanghai

Shanghai offers useful insights into public hospital reforms because it is a very large healthcare market (more than US$14 billion spent in 2011) and is further from the central powers that-be than Beijing, the country’s largest healthcare market. As such, Shanghai offers a better laboratory for reforms and is large and influential enough that if reforms work, there is a high probability other local and provincial governments will emulate the Shanghai model.

Shanghai’s “old” hospital governance model featured lines of authority that tended to emphasize centralization at the expense of local governance that could recognize and adapt to ground-level realities (Exhibit 4). For instance, hospitals owned by the Ministry of Health were directly under the ministry’s jurisdiction.[45] This reduced local administrative leverage, because as former Shanghai Vice Mayor Shen Xiaoming puts it “the simple rule of thumb is, whoever gives hospitals money, the hospitals will listen to them.”

Exhibit 4: Shanghai’s Old Public Hospital Governance Structure

Source: Health Affairs, China SignPost™ analysis

While government funds do not constitute a large portion of public hospital budgets, they are large enough at 6-8% that a threat to that money flow will attract attention in the hospital management suite. Even more to the point, the hospitals will also listen to whoever wields regulatory and approval power over the actions managers want to take. The local authorities largely lacked this power under the old system, particularly if the bricks and mortar building already existed and was furbished, thus removing the potential lever of withholding construction permits.

Shanghai’s public hospital sector reform has taken shape over nearly a decade and yielded a dramatically different organizational chart. The campaign began with the 2005 establishment of the Shanghai Healthcare and Hospital Development Center (申康医院发展中心), a state-owned non-profit legal person (国有非营利性的事业法人) charged with overseeing major decisions and investments made by public hospitals formerly under the MOH’s direct control.[46] The Hospital Development Center now oversees at least 24 public hospitals in Shanghai, including some hospitals affiliated with Fudan University (Exhibit 5).[47]

In 2008, the State Council enabled the establishment of the Shanghai Health Bureau (上海市卫生局) via the Shanghai City People’s Government Structural Reform Plan (上海市人民政府机构改革方案).[48] The Shanghai Health Bureau discharges a wide supervisory mandate, and is specifically tasked with “strengthening supervision of the Shanghai Healthcare and Hospital Development Center according to law.”[49] Local sources suggest the Shanghai Health Bureau plays a more distant supervisory function and that the most direct supervisory hierarchy for the public hospitals in Shanghai under the Hospital Development Center’s authority is (1) Hospital Development Center, (2) Shanghai Health Council, and (3) the Shanghai city government (Exhibit 5). The local SASAC branch also helps supervise investment decisions.

Exhibit 5: Shanghai’s New Hospital Governance Structure

Source: Zheng et.al, Economic Observer

Signs of Greater Local Regulatory Strength

The Hospital Development Center appears to be entering a new and more established and robust phase of operations. One clear point of evidence is the organization’s centerpiece role in a pilot program to create a Chief Accountant Small Working Group that spans hospital bureaucratic lines.[50] As of October 2013, the Hospital Development Center was searching for 18 Chief Accountants, whose responsibilities would include “helping hospital chiefs strengthen internal accounting, economic analysis and monitoring, and management of state assets.”[51] Qualified applicants need to have at least three years’ relevant experience in accounting, auditing, or state asset management.[52] The job listing also specifically notes that applicants should be under the age of 50.[53]

This suggests a clear intent to build a cadre of relatively young accountants who are competent and less likely to have been a product of command and control thought processes. Most importantly, it shows that Shanghai wants to put real expertise and local-level financial analytical capability into the regulatory structure to catch problems early and improve information transparency. There will be capacity questions since so many hospitals regulated by the Hospital Management Center, but building initial capability is an important step on the road to having sufficient capacity, since once capability exists it can be scaled up into greater capacity more easily than capability can be achieved to begin with.

The Hospital Development Center personnel listings also suggest another importance governance development is afoot—a nascent market for professional public hospital management personnel that will become deeper and more dynamic as additional cities join the public hospital reform process. A number of large cities, including Beijing, Chengdu, Kunming, Shanghai, and Shenzhen now have either hospital management centers or municipal hospital management bodies.[54]

These entities’ fundamental administrative purpose and operative functions are similar and as they grow out, will create an increasingly fungible corps of professional managers with the relevant capabilities and experience who can work in a variety of cities. To be sure, this process will have fits and starts.

For instance, nearly 70% of a pool of 173 hospital middle managers surveyed in Wuhan in 2013 said that a lack of separation between ownership and management in public hospitals is the biggest impediment to professionalizing the hospital manager ranks.[55]This suggests two key dynamics: first, deeper guanban fenkai reforms can reinforce professionalization of hospital managements and second, many of the younger hospital managers are either not strongly affiliated with the Party, or even if they are, nonetheless strongly support making public hospitals more independent of the government, a potential positive sign for continued moves toward true corporatization.

So in light of the new ownership and control structure, how “autonomous” are Shanghai’s public hospitals and how close are they to being corporate entities? A recent assessment by researchers from the Ministry of Health, Fudan University School of Public Health, and Shanghai First People’s Hospital speaks to these questions.[56] The researchers applied a set of metrics drawn from Preker and Harding’s seminal work and used them to see how much autonomy public hospitals in Shanghai have under the new control regime relative to the old one (Exhibit 6).

The rights to appoint senior and middle hospital managers, dispose of assets, disposal of residual funds and claims, and to make strategic financial and investment decisions lie at the heart of organizational autonomy and would be rights that most corporate entities would expect to enjoy substantial latitude to exercise. For all four rights, entities above the public hospital level in Shanghai continue to exercise a dominant degree of control. In addition, even for areas such as pricing where hospitals nominally appear to have meaningful authority, the government still exerts a powerful backdoor influence over pricing of procedures, since it can shape how much, and for what procedures, the public health insurance program reimburses.

To be fair, the fact that the dominant degree of control is now localized at the city level in Shanghai denotes significant progress. Yet at the same time, it suggests that true corporatization of public hospitals in the city (and elsewhere in China) most likely is at least 2-3 years down the road, and potentially further.

Exhibit 6: How “Autonomous” Are The Shanghai Public Hospitals?

Source: Zhang et.al, Shanghai Jiaotong University

The Shanghai government’s insistence on keeping its hand firmly on key levers of public hospital operations helps explain investors’ substantial hesitation to enter into public-private partnerships, lest they end up as a modern version of Zhang Jian’s shareholders—along for the ride, but with little to no influence over management despite advancing significant amounts of capital. In short, specialist private hospitals presently offer a more clearly defined legal, political, and economic risk profile.

- What Additional Barriers to Corporatization Do Public Hospitals in China Face?

China’s public hospital system is far from monolithic and managers—particularly the growing generation of relatively apolitical professionals—will likely emphasize their own hospitals, as opposed to a propagandistic ideal of a “greater national good.” So the bottoms-up reform constituency looks increasingly robust. As such, political inertia and resistance from ministerial-level rice bowls comprises the single most significant barrier to corporatization that public hospitals must overcome.

Analysts writing in hospital sector trade publications say that the core challenges for further reforms aimed at separating ownership and management lie in two primary zones. First, what will the Ministry of Health’s relationship with public hospitals be as governance structures evolve and hospitals become more independent from the Central Government? How will the Ministry respond to a set of changes that forces it to begin transitioning from an “omnipotent” regulatory mentality to a more “service-oriented” one where power is devolved away from the center?[57]

It is too early to draw high-confidence conclusions. That said, the fact that Shanghai’s hospitals have been able to transition into their new locally-focused governance structure without undue overt opposition from the central Ministry of Health and the fact that the new governance structures appear to be taking an ever deeper hold suggest a positive future in terms of there being a favorable political climate for public hospital reforms that afford localities and their hospitals greater autonomy. In addition, the Shanghai public hospitals have strong political top cover to continue reforms, as the city’s mayor Yang Xiong stated in May 2013 that public hospital reforms are “difficult” but are also “among the most important.”[58]

Second, will China’s public hospitals be endowed with a robust independent legal personality, and if so, when might this happen and what might catalyze the change? An interpretation of healthcare reform priorities in the 18th Third Plenary Session provided by Xinhua in February 2014 helps provide some clarity as to what relative importance the Central Government attaches to various public hospital reform steps. The hospital-centric portion of the interpretation came before the other three (pricing, diagnostics, and drug subsidies) and noted that along with defining the government’s responsibility for public hospitals and separating ownership and management, reforms should also occur with respect to granting public hospitals independent legal personality (落实公立医院独立法人地位).[59]

Chinese sources currently appear not to specify what forms an independent legal personality for hospitals should take. Some authors from the Institute of Medical Information take the position that none of the country’s four current forms of legal personhood (企业法人、机关法人、事业单位法人、社会团体法人四类) suffice because the public hospital resides in an unusual space where it functions basically as a marketized entity, but also must fulfill important social responsibilities.[60] If this type of view prevails in the policy debate, one potential outcome is that China would need to create a “Hospital Law” that plays an enabling role in the way that the Company Law does, including defining what type of legal personality a public hospital has and what rights this entails.

A more sensible approach would be to corporatize more along the Singapore model analyzed above and make public hospitals “enterprise legal persons” (企业法人) governed by the 2005 Company Law. This would tap into the already substantial body of law and expertise on the Company Law. Enterprise legal persons must meet five core criteria to be recognized under Chinese law and public hospitals could, with sufficient legal tweaks, fulfill these requirements.

Foremost among the logical changes, the Chinese government could enable the creation of fully state-owned hospital holding companies similar to how Singapore has done, which could then step into the shoes of local SASAC branches as the “owner-controllers” of the public hospitals’ physical assets. There is already at least one precedent in a national-scale city—Chengdu—for diluting local SASAC power over hospital assets. In Chengdu, the recently created Hospital Bureau that supervises public hospitals is independent of the local SASAC branch.[61]

First, the enterprise legal person must be approved and recognized by a competent authority.[62] Second, it must possess its own property.[63] This could be accomplished via the holding company, as Singapore has done with MOH Holdings and its subordinate companies, SingHealth and NHS. Third, the enterprise legal person must possess its own name, organizational structure, and premises.[64] Again, the corporate holding structure coupled with the hospitals’ existing names and premises would fulfill this requirement. Fourth, the enterprise legal person must be able to independently assume civil legal obligations.[65] The holding structure would allow this, while simultaneously providing a pathway for the state to maintain full control over important social assets. Fifth, the enterprise legal person must have the capacity to engage in civil legal actions, of which a corporatized hospital would presumably be capable.[66]

- Conclusion: Corporatize Now Based on National Guidelines, or Face Major Problems Down The Road

While Beijing is clearly doing its best to exit the direct public hospital management business (yet again), the political credibility buck ultimately stops at the national level if provincial and local problems and dissatisfaction with public hospital services become sufficiently serious. And with that in mind, events may begin to force policymakers’ hand if they do not move decisively to corporatize, or at least more clearly define the legal status of public hospitals in China. There are a sizeable number of local deals—primarily in 2nd and 3rd-Tier cities—where investors are taking majority stakes in public hospitals (typically ones suffering from some type of financial problems), with local governments as the minority partner.[67]

As such deals proliferate, there is a rising sentiment that these hospitals are actually “privatized” once the investment capital comes in, even if they still must fulfill the same social functions that their MOH-owned predecessors did. And the ground level reality is that in practical terms, their behavior (pricing and service offerings) will change fast at the expense of patients who in some areas may not have many other options for obtaining medical services they can afford.

A broad empirical study of U.S. hospital behavior suggests that public hospitals are “the most likely to supply the unprofitable services that are disproportionately needed by poor and underinsured patients,” which typically makes them “caregivers of last resort.”[68] The U.S. experience is primarily driven by economic forces that largely transcend the otherwise formidable differences between the U.S. and Chinese healthcare ecosystems. What’s more, in the Chinese context, public hospitals are likely to be the caregivers of first and last resort, making them even more important to the bulk of the population, which will likely not be able to afford care at specialist private facilities which are profit-driven.

The fact that local governments are becoming actual shareholders in the hospitals also raises problems because the government previously managed hospitals with an eye to service (and cost-minimization), as opposed to profitability, which engenders a much different range of incentives that run counter to providing a broad spectrum of care at affordable prices. These potentially massive conflicts of interest are largely hidden now, but would likely assert themselves rapidly in the event of an economic slowdown that made dividends and income from local hospital operations a more important source of government financing than they are now.

For the central, or even provincial, governments to try and unwind this growing tangle of informal local “corporatization” and “privatization” of public hospitals would be a major drain of funds and political bandwidth. Yet the problems could be pre-empted by adopting a system whereby hospitals were officially corporatized based on national-level guidelines and laws, but à la Singapore, remain public institutions, perhaps with non-profit status.

The bottom line: China’s public hospital reform experiments thus far have laid a foundation for corporatization that is stronger than many observers believe. Public hospitals now are where the SOEs were in the 2-3 years before the 1994 Company Law was promulgated. Chinese leaders need to act soon to lay down additional, corporatization-specific ground rules for public hospital reforms moving forward. Without national guidelines on corporatization of hospitals, Beijing risks either (a) having public hospitals being privatized and perpetuating the skewed incentives that have helped spark social unrest and prompted the 2009 reforms in the first place or (b) having such a lack of legal clarity that investors balk at providing the full volume of capital that China badly needs in order to avoid having the public hospital system become a substantial drag on the national balance sheet.

[1] Lan Fang, Li Yan, Luo Jieqi, Ren Zhongyuan Lin Jinbing and Han Xiaomei. “Anger and Angst in Hospitals Where Doctors Die,” Caixin, 20 November 2013,http://english.caixin.com/2013-11-20/100607242.html

[2] Ruth E. Brown, Dionisio Garcia Piriz, Yuanyuan Liu, and Jonathan Moore. “Reforming Health Care in China,” April 2012, http://sites.fordschool.umich.edu/china-policy/files/2012/07/PP_716_Final_Policy_Paper_Health-Final.pdf (21)

[3]Tsung-Mei Cheng, “Explaining Shanghai’s Health Care Reforms, Successes, And Challenges,” Health Affairs, 32, no.12 (2013):2199-2204

[4] Gabe Collins and Andrew Erickson, “China’s S-Curve Trajectory: Structural factors will likely slow the growth of China’s economy and comprehensive national power,” China SignPost™ (洞察中国), No. 44 (15 August 2011).

[5] M. Ramesh, Xun Wu, and Alex Jingwei He. “Health Governance and Healthcare Reforms in China,” Health Policy and Planning 2013; 1-10. Doi:10.1093/heapol/czs109.

[6] World Bank Development Indicators, World Bank, http://data.worldbank.org/data-catalog/world-development-indicators. Also, to be sure, years of war and revolutionary turmoil likely helped “pad” the baseline for these numbers, but they nonetheless represent a remarkable improvement.

[7] Madhurima Nundy and Rama Baru, “Recent Trends in Health Sector Reforms and Commercialization of Public Hospitals in China,” ICS, 2013, Paper 12, Vol.2.

[8] Cao Yanlin, Wei Zhanying, Wang Jiangjun, “Discussion on Public Hospitals’ Independent Legal Status,” (公立医院独立法人地位探讨), Chinese Hospitals, Vol.14, No.12, 2010. (18-19)

[9] Ramesh 3

[10] Zhe Dong and Michael R. Phillips, “Evolution of China’s Health Care System,” The Lancet, Vol. 372, November 2008. (1715)

[11] Wei Zhang and Vicente Navarro, “Why hasn’t China’s high-profile health reform (2003−2012) delivered? An analysis of its neoliberal roots,” Critical Social Policy 2014 34: 175 originally published online 23 January 2014. DOI: 10.1177/0261018313514805.

[12] Vivian Lin, “Transformation in the healthcare system in China,” Current Sociology 2012 60:427, DOI: 10.1177/0011392112438329.

[13] Sarah L. Barber, Michael Borowitz, Henk Bekedam, and Jin Ma. “The hospital of the future in China: China’s reform of public hospitals and trends from industrialized countries.” Health Policy and Planning 2013: 1-12. Doi: 10.1093/heapol/czt023.

[14] See, for example: Shanghai Changning District Central Hospital Joint Venture Contract,http://www.sec.gov/Archives/edgar/data/922717/000092271702000002/contractualjvcontract.htm, and Shanghai Fosun Pharmaceutical (Group) Co. DISCLOSEABLE TRANSACTION ACQUISITION OF 60% EQUITY INTEREST IN CHANCHENG HOSPITAL,http://www.hkexnews.hk/listedco/listconews/sehk/2013/1009/LTN20131009561.pdf

[15]Li Weiping and Huang Erdan (李卫平, 黄二丹), “The Path and Strategy for Making Public Hospitals Into Independent Legal Entities,” (实现公立医院独立法人地位的途径和策略), Health Economics Research Institute (卫生经济研究), Vol. 11, 2010.

[16] Song Lingxia and Jiang Hong, “The Exploration about Public Hospitals Corporate Governance Structure in China,” (我国公立医院法人治理结构模式探索). Value Engineering (价值工程). Issue 25, 2012.

[17] Anqiu City People’s Hospital Asset Transfer Agreement,http://www.sec.gov/Archives/edgar/containers/fix170/1277425/000104746905003737/a2151652zex-10_22.htm

[18] Golden Meditech, Business Overview,http://www.goldenmeditech.com/eng/business/overview_b.php (accessed 20 April 2014).

[19] China Sinopharm Intl Corporation, Products and Services, Hospital Management,http://www.sinopharmintl.com/nr/cont.aspx?itemid=37&id=122. (accessed 20 April 2014).

[20]新乡市市直事业单位法人信用等级评定结果公示, 28 January 2013,http://www.xinxiang.gov.cn/sitegroup/root/html/4028815814acaf060114acb5c05d002a/20130128165615831.html

[21] 公立医院集团化改革 新乡5家医院踏上央企快车, 20 June 2013, 东方今报http://www.jinbw.com.cn/jinbw/xwzx/zzsx/201306201176.htm (accessed 20 April 2014).

[22] Company Prospectus, November 2013, Pg. 138 (copy on file with author)

[23] April Harding and Alexander Preker, “Understanding Organizational Reforms,” World Bank, September 2000,http://www.who.int/management/facility/hospital/Corporatization.pdf

[24]“Vice Health Minister Says: Public Hospital ‘Legal Personalization” Reforms Should Avoid ‘Corporatization,’”(卫生部副部长:公立医院”法人化”改革应避免”公司化”), Xinhua, 30 October 2009, http://news.xinhuanet.com/politics/2009-10/30/content_12358519.htm

[25]“Private Capital Shuns County-Level Hospitals While Second and Third-Level Public Hospitals are Investment Hot Spots,” (民资冷落县级公立医院 二甲三乙医院成投资热点), China.com, 28 February 2014,http://finance.china.com.cn/industry/medicine/yyyw/20140228/2220403.shtml

[26] “Autonomization/Corporatization,” World Bank,http://web.worldbank.org/WBSITE/EXTERNAL/TOPICS/EXTHEALTHNUTRITIONANDPOPULATION/EXTHSD/0,,contentMDK:20190817~menuPK:438810~pagePK:148956~piPK:216618~theSitePK:376793,00.html, accessed on 25 April 2014.

[27] Fixing the Public Hospital System in China,” World Bank, China Health Policy Notes,http://siteresources.worldbank.org/HEALTHNUTRITIONANDPOPULATION/Resources/281627-1285186535266/FixingthePublicHospitalSystem.pdf

[28] Ibid.

[29] April Harding and Alexander Preker, “Understanding Organizational Reforms,” World Bank, September 2000,http://www.who.int/management/facility/hospital/Corporatization.pdf (6)

[30] Ministry of Health and Welfare, 2012 Hospitals,http://www.mohw.gov.tw/EN/Ministry/Statistic_P.aspx?f_list_no=474&fod_list_no=3905&doc_no=29655

[31] Don Shapiro, AmCham Taipei, “Examining Taiwan’s Hospitals,”http://www.amcham.com.tw/topics-archive/topics-archive-2009/vol-39-no-3/2696-cover-story-examining-taiwans-hospitals

[32] Ibid.

[33] M. Ramesh, “Autonomy and Control in Public Hospital Reforms in Singapore,” The American Review of Public Administration 2008 38:62. DOI: 10.1177/0275074007301041.

[34] Ibid. 67

[35] Ibid. 67

[36] Ramesh 70

[37] Ibid.

[38]“Analyzing the Medical Sector Reforms—2009 Marks the Start of Public Hospital Reform,” (医改方案解读——公立医院改革2009年开始试点), Xinhua, 14 April 2009,http://news.xinhuanet.com/politics/2009-04/14/content_11184470.htm

[39] Wang Hufeng (王虎峰), “Public Hospital Reform: Assessing Achievements and Development Trends,” (公立医院改革:阶段性成果和发展趋势), China Medical Insurance (中国医疗保险), Issue 5, 2013. (25)

[40] Ibid. 6.

[41] Ibid. 6.

[42] “Administration,” Huashan Hospital, http://www.huashan.org.cn/roomcontent/261

[43] “Opinion Regarding The Implementation of Social Harmony management Work,” (关于加强医院社会治安综合治理工作的实施意见), Leshan Hospital, 31 March 2008,http://www.leshan-hospital.com.cn/viewgovarticle.asp?id=40

[44] Geng Xiao, “Reforming the governance structure of China’s

state-owned enterprises,” PUBLIC ADMINISTRATION AND DEVELOPMENT

Public Admin. Dev. 18, 273±280 (1998). http://www.econ.hku.hk/~xiaogeng/research/Paper/PAD-Chinese%20SOE%20governance.pdf

[45] Tsung-Mei Cheng, “Explaining Shanghai’s Health Care Reforms, Successes, And Challenges,” Health Affairs, 32, no.12 (2013):2199-2204, 2201.

[46] Shanghai Healthcare and Hospital Development Center, “About Us,”http://www.shdc.org.cn/shenkang.action

[47] Zhang Donghui, Tu Shiyi, and Xue Di, “Analysis of the Responsibilities and Authorities in Governance Structure of Public Hospitals in Shanghai City,” (上海市公立医院治理结构的职能和权力分析), Chinese Hospital Management, 2012, 32(3):9-11

[48] “Shanghai City Health Bureau,” Shanghai Government, http://www.shanghai.gov.cn/shanghai/node2314/node2319/node2405/node3641/

[49] Ibid.

[50]“Regarding the Communication on the ‘Shanghai City Level Public Hospital Chief Accountant Pilot Management Program,’”(关于印发《上海市市级公立医院总会计师委派管理试行办法》的通知), Shanghai Finance Bureau, 19 March 2013,http://www.czj.sh.gov.cn/zcfg/gfxwj/kjl/qtkjl/201303/t20130319_141323.html

[51]Shanghai Healthcare and Hospital Development Center Job Posting (上海申康医院发展中心公开招聘), 9 October 2013, www.shdc.org.cn

[52] Ibid.

[53] Ibid.

[54] See for example, Beijing Municipal Hospital Administration, http://www.bjah.gov.cn/, also Public Hospital Administration of Shenzhen Municipality,http://www.szpha.com/szpha/view?id=2, and finally, Chengdu Hospital Authority,http://www.cdyg.gov.cn/. (All accessed 27 April 2014)

[55] Yao Hongwu, Fang Pengqian, and Xie Jinliang, “Specialization of Directors in Public Hospitals: Hospital Middle Managers’ Cognition and Revelation,” (公立医院院长职业化: 中层管理者的看法于启示), Chinese Hospital Management(中国医院管理), Vol.33, No.9, September 2013. (54)

[56] Zhang Donghui, Tu Shiyi, and Pan Changqing, “Analysis of Shanghai’s public hospital governance structure with the Preker-Harding model,” (利用Preker-Harding 模型分析上海市公立医院治理模式), Chinese Health Resources, Vol.1, Jan. 2013. (43-44)

[57] Zhang Guimin (张贵民), “Ownership and Management are Tough to Separate,” (管办难分), China Hospital CEO, Z1, 2013. (47-48).

[58] “Shanghai Mayor Says Public Hospital Reforms Are Among the Most Important,” (公立医院改革是医改重中之重杨雄主持市府常务会部署三年行动计划强调让群众真正感受到实惠), 7 May 2013, http://www.gov.cn/gzdt/2013-05/07/content_2397106.htm

[59]“Analysis: How to Speed Up Public Hospital Reforms and Encourage Social Management of Medicine,” (解读:如何加快公立医院改革和鼓励社会办医), Xinhua, 14 February 2014, http://www.gov.cn/jrzg/2014-02/14/content_2599665.htm

[60] Cao Yanlin, Wei Zhanying, Wang Jiangjun, “Discussion on Public Hospitals’ Independent Legal Status,” (公立医院独立法人地位探讨), Chinese Hospitals, Vol.14, No.12, 2010. (18-19)

[61] “Chengdu Creates a Hospital Management Bureau that is Independent From SASAC and is Equal to the Local Health Bureau,” (成都设立医院管理局 既独立于国资委又平行于卫生局), People’s Daily, 21 May 2012, http://politics.people.com.cn/GB/17939324.html

[62] Zhao Zhongfu, “Enterprise Legal Persons: Their Important Status in Chinese Civil Law,” Law and Contemporary Problems, Vol.52, No.3, Summer 1989. (5-9)

[63] Ibid

[64] Ibid

[65] Ibid

[66] Ibid

[67] See for instance, “Xuzhou Third People’s Hospital Reforms By becoming For-Profit as Sanbao Group Takes an 80% Shareholding,” (徐州第三人民医院改制营利性 三胞集团控股80%), Sohu, 25 April 2014, http://roll.sohu.com/20140425/n398808719.shtml; also, “Kunming Children’s Hospital Reforms, Changes its Path, and is No Longer a Public Hospital,”(昆明儿童医院改制路崎岖 已不是公立医院), Healthcare Report, 17 June 2013,http://health.takungpao.com/q/2013/0617/1694119.html

[68] Jill R. Horwitz, “Making Profits and Providing Care: Comparing Non-Profit, For-Profit, and Government Hospitals,” Health Affairs, 24, no.3 (2005): 790-801.

")

")

")

")

Development: Drivers, Trajectories and Strategic Implications")