China SignPost™ 洞察中国 Presentation: “Pandemic & Price War: Early Energy Market Insights from the 2019-20 Wuhan Coronavirus Outbreak”

Gabriel B. Collins, “Pandemic and Price War: Early Energy Market Insights From the 2019-2020 Wuhan Coronavirus Outbreak,” Research Presentation, China SignPost™ (洞察中国), 20 March 2020.

Click here to download full slide deck.

Executive Summary

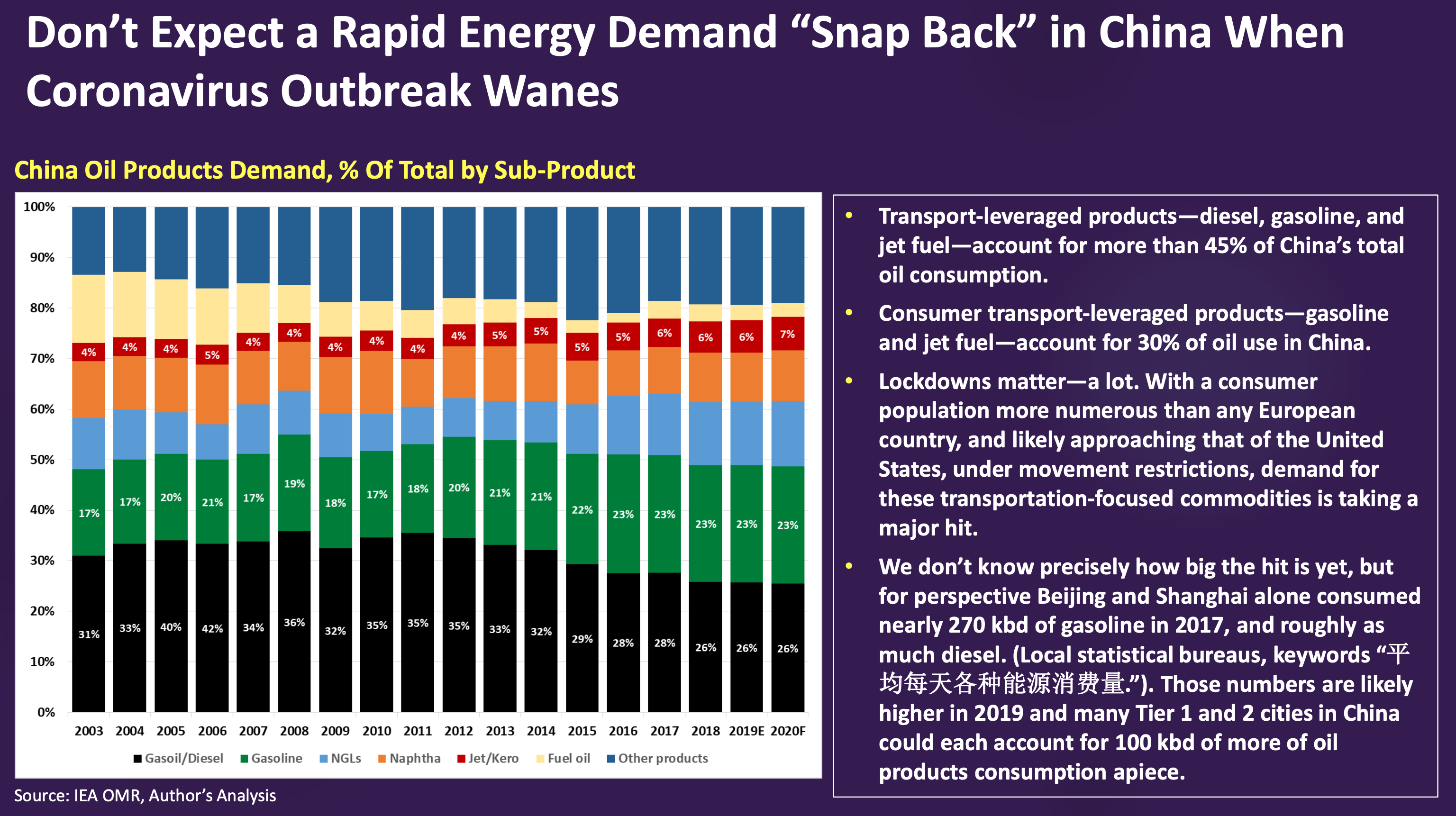

- The coronavirus is likely the biggest global oil demand shock for China and other major industrial powers in the past 50 years, exceeding even the impact of the 2008 Global Financial Crisis. This risk is magnified by the fact that the massive 2009-10 China stimulus measures, which drove an oil demand increase of approximately 1 million bpd, are likely not in the cards this time around.

- Oil use foregone during the lockdown period is most countries likely will not be recouped and it will likely take multiple quarters for demand to attain pre-pandemic levels. This is likely to be especially true for air travel, one of the most discretionary forms of consumer oil use. One potential offset could come through consumers eschewing planes and trains and using personal cars for a greater share of inter-city travel. Personal car use is generally significantly more oil-intensive per capita than flying on a plane.

- At the same time, Saudi Arabia has declared an oil price war on Russia and Moscow wants to suppress U.S. shale. Russia can likely sustain the price war through the remainder of 2020 and I think the Saudis will blink first. That said, several tough quarters lie ahead.

- Keep your head up! The economic restart and recovery will take time and feature fits and starts as supply chain kinks are worked out, but the underlying physical infrastructure remains intact and can be switched back on fairly quickly. In that respect, Covid-19 is very different than a natural disaster that physically disrupts and destroys key assets. Critical basic services such as water, gas, power, and internet services will likely remain available even if the infection burden gets much worse.

- Pandemic disruptions are rooted in our natural human fear response—and in the fact that some proportion of the population may become sick and temporarily unable to function (or even suffer longer-term disability or death). The virus attacks our confidence and strains our institutions, but leaves physical assets untouched.

- We will recover, but the architecture of our commercial intercourse and consumption patterns could be altered for some time. The near-term downturn will likely be deeper than what happened in 2008-09. It’s going to be volatile and challenging through 2020, and perhaps into the first quarter of 2021.

Pandemic and Price War: Early Energy Market Insights From the 2019-2020 Wuhan Coronavirus Outbreak

")

")

")

")

Development: Drivers, Trajectories and Strategic Implications")